Our Shipley Energy Commercial Solutions Team is excited to share with you the August Energy Market Update to keep you informed on trends, weather, and other factors impacting the energy market.

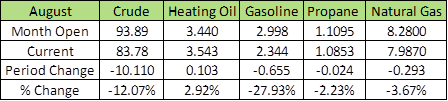

Energy futures prices decouple from physical cash basis markets – distillate rallies, gasoline crumbles while crude slides.

Why it is important: OPEC+, the world’s largest oil cartel, controls the majority of the world’s oil output. They have already voiced concerns over wide price disconnects between the futures and physical markets. If global recession risks, which have steadily showed up in the futures prices, impact cash market demand, they may elect to cut crude oil production in an already very tightly supplied market. Analysts project this could potentially send prices rallying back to $115-120 per barrel this year if OPEC leaves the door open for further supply cuts.

Why it is important: If signed, this deal would allow Iran to immediately sell an estimated 70-100 million barrels of oil into the global marketplace, helping alleviate tight supplies which are keeping prices elevated

Why it is important: The removal of this reserve supply further exasperates an already tight market, while reserves must be replenished. Net 2-million-barrel swing, with demand data starting to rebound

Why it is important: The White House and Secretary of Energy, Jennifer Granholm, have voiced serious concerns of days of available supply for heating and transportation. A ban in principle would curb domestic exports but could upset global supply chains, negating the intended effect

Why it is important: China, the world’s largest crude consumer, have locked down many cities due to Covid. When lockdowns are lifted, demand is expected to spike.

We have been prompting customers to prepare during this summer for the potential of higher distillate demand this fall/winter. Front month heating oil futures lows of $3.1424 were the lowest price levels not seen since April. Last month, we advised that $3.00-$3.25 would remain very solid support and should be bought. A quick and strong reversal off these levels brought the upper end of the $4.15/gal range, which coordinated with major levels of the 2008 highs. Recent profit taking to end the month sent heating oil prices back down to $3.45/gal and have since rallied 20 cents as October has become the front month contract.

Northeast spot market physical diesel and heating oil remains a serious concern this winter, with exports still drawing ample supply out of the U.S., especially the Northeast where it is needed most. Any refining and pipeline supply disruptions could cause volatile basis price spikes like the market witnessed this past winter of $1.00 or more. Please work with your Shipley adviser to discuss some strategies we are suggesting with our customers to mitigate these risks, protect your supply, and budgets.

Over the past month of natural gas Nymex trading, the September 2022 Nymex contract continued the trend of volatile trading bouncing between a range of $7.62/MMBtu on August 1st and reaching as high as $10.02/MMBtu by August 23rd.

The September contract finally settled at $9.353/MMBtu following last month’s August 2022 settlement price of $8.687. This continues a two-month trend of higher month-to-month Nymex settlement prices as energy markets around the world remain high-priced and unpredictable.

Trading over the past two weeks has also been influenced by the announcement that the currently offline Freeport LNG (liquified natural gas) export facility in Texas will remain offline until at least November 2022. This will continue the availability of up to 2 BCF (billion cubic feet) of natural gas per day domestically that would otherwise have been sent into global LNG markets in Europe and Asia.

Despite this additional available supply, natural gas futures have shown continued price strength trading in a range between $8-$10/MMBtu.

There are several factors impacting the natural gas markets currently:

Even with natural gas futures prices on the rise again, there are still opportunities to lock in longer renewal terms in the 24–36-month range at better pricing. Futures pricing beyond March 2023 drops down below $6, compared to prices in the near term (October ‘22-March ‘23) reaching above $9. Ask your Account Manager about 24–36-month renewal options to take advantage of lower prices in further out months.

Other options include Basis Only or Nymex Lock deals to separate the two elements of your natural gas price to look for potential value vs standard Fixed pricing. Reach out to your Account Manager today for details.

September 2022 Natural Gas NYMEX Settlement Price: $9.353/MMBtu

Last month: August 2022 Natural Gas NYMEX Settlement Price: $8.687/MMBtu

Last year: September 2021 Natural Gas NYMEX Settlement Price: $4.370/MMBtu

One strategy that continues to cost customers money is the “wait and see” approach. This has not proven at all effective for the last year, outside of a two-day freak occurrence drop in late June 2022. Below are some sobering benchmarks for the 12-month forward PJM electricity curve:

Wholesale prices, while volatile day-to-day, are consistently trending upwards. Getting an early start on developing your energy buying strategy continues to result in lower rates and less energy spend. Allowing your business to be backed into a corner and forced to make a poorly timed buy at the last minute is a sure way to pay more.

Disclaimer: The market update is intended solely for informational purposes only. Shipley Energy Company does not warrant or attest to its accuracy. All actions and judgments taken in response to this report are the recipient’s sole responsibility. Shipley Energy Company shall not be liable for any direct, indirect, incidental, consequential, special, or exemplary damages or lost profit resulting from these market updates.