The Shipley Energy Commercial Solutions Team is excited to share the October Energy Market Update to inform you of trends, weather, and other factors impacting the energy market. Read the September 2023 energy market update here.

Skip to:

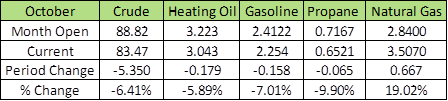

The November 2023 NYMEX Natural Gas contract expired at a price of $3.164/mmbtu. That is down 39% from last year’s historically high November settlement price of $5.186/mmbtu. The November 2023 settlement marks the tenth month in a row that the NYMEX price has settled below $4 following the January 2023 settle price of $4.709. The period from October 2021 to January 2023 saw NYMEX prices skyrocket to as high as $9.35 on concerns of supply chain disruptions and global gas shortages.

As we enter the start of winter, we are still maintaining above average levels of natural gas available in storage to meet winter heating demands. The level of gas available in underground storage is currently nearly 8.5% higher than last year at this time and about 5% higher than the 5-year historical average.

Entering winter with storage above historical average levels bodes well for the outlook of meeting heating demands domestically when the coldest days of the year arrive. Ample supply in storage eases concerns of supply shortages during critical times of heating demand, which should work towards keeping NYMEX market prices stable and avoid spikes to higher levels.

In the short term, an early cold shot has much of the eastern and midwestern U.S. under freeze warnings to end October and start November. Temperatures near freezing this early in the winter will likely prompt an above average withdraw of storage gas in the coming weeks. This will be a trend to watch over the next few months since market traders may become more concerned for a potential for shortage of supplies if storage levels are depleted before the most typically frigid winter months of January and February.

Factors Impacting the Natural Gas Markets Currently:

Action Advice:

As we enter winter, now is the time to lock in fixed natural gas rates while NYMEX prices for the next 12 months remain in the low to mid-$3 range. Act now to lock in low fixed natural gas supply rates for the next 6-12 months for the lowest current price offers before the coldest days of winter.

Other rate options include Basis Only or NYMEX Lock deals to separate the two elements of your natural gas supply price to look for potential value vs. standard Fixed pricing. Ask your Account Manager for details.

November 2023 Natural Gas NYMEX Settlement Price: $3.164/mmbtu

Last month: October 2023 Natural Gas NYMEX Settlement Price: $2.764/mmbtu

Last year: November 2022 Natural Gas NYMEX Settlement Price: $5.186/mmbtu

Electricity edged upward as we moved through an unseasonably warm October and one month closer to winter. The PPL forward 12-month curve slightly increased from 4.58 to 4.70 cents per kWh, however it’s another hole in the dam of clients who have held out while insisting that rates should return to the 23-year lows of 2020.

Our position on the market is essentially “don’t bet it all on mid-November.” December-February starts who have rejected offers in September and October to be rewarded with the occasional 2% down-day are playing with fire as winter draws closer; the potential for the market to increase by 30% is far greater than the likelihood of it dropping 15%. If you’re renewing this winter and are still holding out, we recommend taking action.

The recent forecast for a below-average winter, the quickly-expanding LNG network that will double in the next five years and cannibalize domestic supply, the quickly-growing fleet of EV’s that will well outpace electric supply capability, and the two wars happening right now are all extremely bullish factors that should encourage any “fix it all at once” buyer to take ’24 and ‘25 off the table right now.

The time to lock winter starts is now or you’re essentially already accepting real-time risk. Those who recognize the dominance of the bullish market factors will lock out as far as suppliers will let them.

Action Advice:

October was impacted by numerous headlines and factors whipsawing price action. The first half of October saw a break below $3.00 HO support as numerous recessionary headlines and data came across. As we have been seemingly discussing for over a year now, interest rates continued to rise which has continued to help put a clamp on economic expansion. Economies around the world are now grappling with the highest interest rates imposed by central banks in over 15 years. ISM manufacturing data has continued to contract, while inflationary data continues to rise.

This data has directly clashed with diesel and heating oil supply on hand, which are at a staggering -20 million barrels below the 5 year average. All of this coming into a period of increasing cool weather demand. The industrial recessionary demand vs. low supply picture will continue to clash. Ultimately demand will win out and prices could see a substantial rally when industrial demand turns higher.

Action Advice:

We have seen an increased fixed price as the front end of the heat curve has rallied, increasing the backwardation in the market. The closer to winter and next year, the back end of the winter strip curve will start to become more volatile and historically move more closely with the front month. As volatility increases the premium for such contracts will increase as well. The consensus is that there will not be a repeat of the unusually warm winter last year which helped contain prices. We are bullish HO futures above $2.92 and $3.00 and become more bullish above $3.06 to $3.14. Our recommendation is $2.92 support (Ukraine War breakout price) has consistently held and is a good area to consider getting long against.

Please speak with your Shipley Energy Fuels Advisor to help your business navigate the current market.

Disclaimer: The market update is intended solely for informational purposes only. Shipley Energy Company does not warrant or attest to its accuracy. All actions and judgments taken in response to this report are the recipient’s sole responsibility. Shipley Energy Company shall not be liable for any direct, indirect, incidental, consequential, special, or exemplary damages or lost profit resulting from these market updates.